Whether you’ve sold your company, inherited a large sum of money or properties, or won the lottery, coming into wealth in New Zealand can come with a lot of emotional, mental, and financial baggage.

You might be elated one moment, despondent the next, terrified you’ll lose it all, excited for what the future holds, worried that now you have to invest it and make it last forever. The tall poppy syndrome that is prevalent in many corners of NZ society may also hold you back from celebrating your victory or expressing gratitude for the parents that left you a fortune.

This is opportunity to change your life for the better. It may also be a change to change your family’s, children’s, spouse or partner’s life for the better as well.

Here is a tactical financial checklist to help you navigate achieving significant wealth in New Zealand.

- Tax planning: Engage with a tax advisor who focused on high-net-worth (HNW) clients

- Estate planning and trusts: a basic will and estate structure to get your started

- Insurance: Ensure that your home, contents, and auto policies are updated and paid up. We’ll think about life insurance later.

- Asset allocation: Decide on an intentional and thoughtful portfolio allocation. Speak with a fee-only, independent financial advisor that can give you unfiltered advice.

Tax Planning

New Zealand has a simple tax regime. No general capital gains tax. No inheritance tax. No gift duty. This is good and means you don’t need a much tax advice.

The FIF or Foreign Investment Fund Tax causes some anxiety among HNW and high-income investors, but you shouldn’t let the tax tail wag the investment dog.

Portfolio Investment Entities, or PIE funds, represent an opportunity for HNW investors to cap their tax on dividends and interest income at 28%.

Estate Planning and Trusts

Trusts are a tool that can be used for two main purposes: tax optimization or asset protection. Because of recent changes to NZ tax law, NZ trusts are rarely used for tax optimization anymore because of the 39% tax on undistributed trust income.

Trusts are still useful for asset protection and relationship-property planning as well as succession planning, but be aware of the 39% trustee rate.

In general, most HNW families can simply and easily create a solid estate plan with a few documents, certified by a trusted lawyer for less than $10,000:

- A will for both partners

- Enduring powers of attorney for property and personal care and welfare for each partner

- An advanced care directive

- A contracting out agreement, especially if entering into relationships with unequal contributions

- A letter of wishes

- An emergency document listing insurance documents, accounts and locations, and core passwords

Insurance

Ensure that your home, contents, and auto insurance are reflective of your current circumstances and are paid up. Also, if you are a business owner

In regards to life insurance, if you have hit a “enough” number, you probably no longer need life insurance. If you are on the younger side and your investments are less liquid, perhaps a $1 million policy on you and/or your partner to provide some transition capital were you to die young may be good.

Insurance is a tool to mitigate risk on potentially catastrophic scenarios. On average, when you buy insurance you lose. That’s how insurance companies make money, they play the averages, like a casino.

Skipping insurance on small expenses, things you can sell insure from your assets, means saving money.

New Zealand is blessed with a decent public health care system and an accident compensation scheme known as ACC, the Accident Compensation Corporation.

Private health insurance is a luxury, and usually unnecessary in NZ. I encourage my HNW to consider the cost of private health insurance. Generally, it is small portion of their budget for a tremendous peace of mind, and many of my HWN clients choose to opt into private health insurance in New Zealand.

Asset Allocation

Building a low-cost, automated, diversified, and simple asset allocation is the single most important thing you can do to preserve, grow, and continue to build your wealth for yourself and future generations to come.

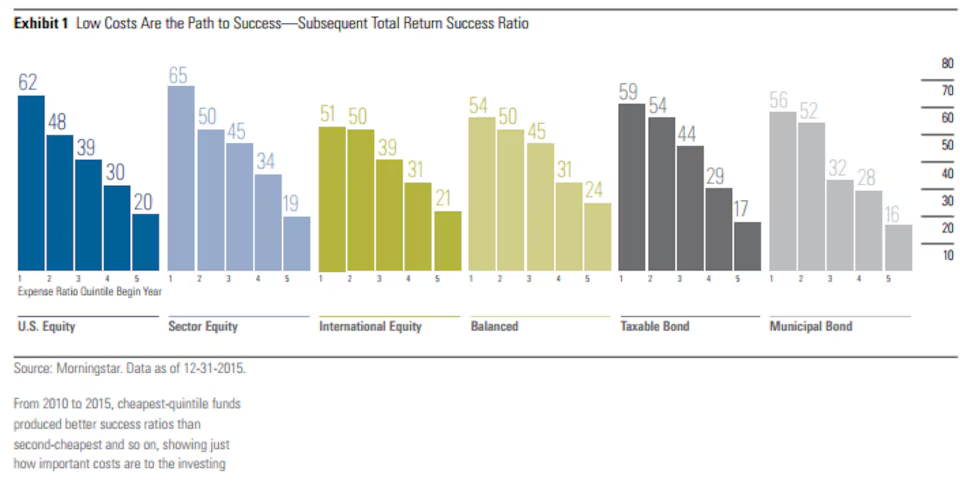

The following chart from Morningstar shows how the cheapest 20% of funds in the US in 2010 both survived and outperformed their category group over the 5 years to 2015. So if you were presented with 10 funds to choose from, the smart money would just pick the cheapest fund and move on with your life. That’s why keeping costs low matters so much. It’s just more money in your pocket, it increases the chance you’ll survive and outperform your competition.

When predicting future investment returns, the most important predicters of success are things within your control:

- Low-cost: Keeping investment costs low

- Automation: Setting up an automated investing plan

- Diversification: Avoiding concentration of investments in one company, sector, asset class, or country

- Simplicity: Complex gets broken easily and is a fragile system. You want to build antifragile systems that are resilient to any market conditions.

As you grow your wealth, there will be a constant pull to complexity. This complexity is unnecessary to achieving most lifestyle goals. It adds stress, friction, costs, and takes up mental bandwidth to juggle the complex financial system you create. You do not need to do this to achieve your financial goals.

A simple asset allocation of cash, real estate, global shares, and global bonds can provide the low-cost, automated, diversified, and simple investment strategy you need to meet your immediate spending needs, your short-term objectives, and your long-term wealth building dreams of legacy, generational wealth, and living the good life.

If you’re new to wealth, and want to speak to an independent, fee-only financial adviser based in Tauranga, New Zealand, book a no obligation, free 30 minute chat with me here. I look forward to helping you navigate your success.