“Why is it so hard to find a good financial adviser?”

I think it should be Simple to find a financial adviser aligned with your interests. That’s why I started Simple Money.

I don’t have any financial products to sell or earn any commissions on products. You pay for the advice. That’s it. That’s Simple.

Simple Money is an independent financial planning firm, offering unbiased, conflict free advice and financial plans for Kiwis of all ages and life stages.

I’ll work with you to learn about your financial situation, understand your goals, build a simple plan, and help you action it.

Kia ora, I’m Spencer Reese.

I started Simple Money because I believe that financial advice in New Zealand is too confusing. Most people’s financial situation can be simple.

Success with money comes down to 2 simple ideas:

Spend less than you earn

Invest the difference early and often

That’s about it.

Keeping your money plan low-cost, automated, diversified, and simple gives you the highest probability of reaching your financial and life goals.

Book a 100% free, 30 minute introductory call with me using the form above.

Problems Solved

Getting Started Investing

Perfect if you just got a promotion, started working, are combining incomes, or are ready to have your money work for you.

Life Milestones

Navigate combining finances after marriage, a new child, or managing an inheritance while looking after family.

Portfolio Review

We help you choose the correct investments, set a reasonable asset allocation, and ensure you truly understand your risk.

KiwiSaver Optimization

We ensure your KiwiSaver is structured for growth, not stagnation, over the course of your working years.

The Holistic Financial Plan

A full review of your entire financial picture, providing a clear roadmap to your life goals.

Cash Flow & Coaching

Design a spending plan that aligns with your values. We help you automate your savings and eliminate financial stress.

How We Can Work Together

Two straightforward options. No commissions, no ongoing fees, no surprises.

One Hour Consultation

One-time fee. No ongoing costs.

Holistic Financial Plan

One-time fee. No ongoing costs.

Problems Solved

- Getting started investing: if you just got a promotion, just started working, are combining incomes, or are ready to start having your money work for you rather than you work for your money.

- Life milestones: Navigating combining finances with your partner after a marriage, child, death in the family, looking after elderly family members, we can look at all of that

- Investment portfolio review: We can help you choose the correct investments for your individual situation, set a reasonable asset allocation, and help you understand risk.

- KiwiSaver: We ensure that your KiwiSaver is set to grow, not stagnate, over the course of your working years

- The Holistic Financial Plan: We’ll review your entire financial picture and provide a road map to achieving your financial goals

Who is Spencer?

- Bachelor of Arts in Economics from Boston University

- New Zealand Certificate in Financial Services (Level 5) from Massey University

- Graduate Certificate in Financial Therapy from Kansas State Univesrity

- Registered Financial Advice Provider (FSP 1009459)

- Former US Air Force and commercial pilot

- Podcast host, author, and owner of a popular personal finance and investing website for US military families

The LADS Investing Principle

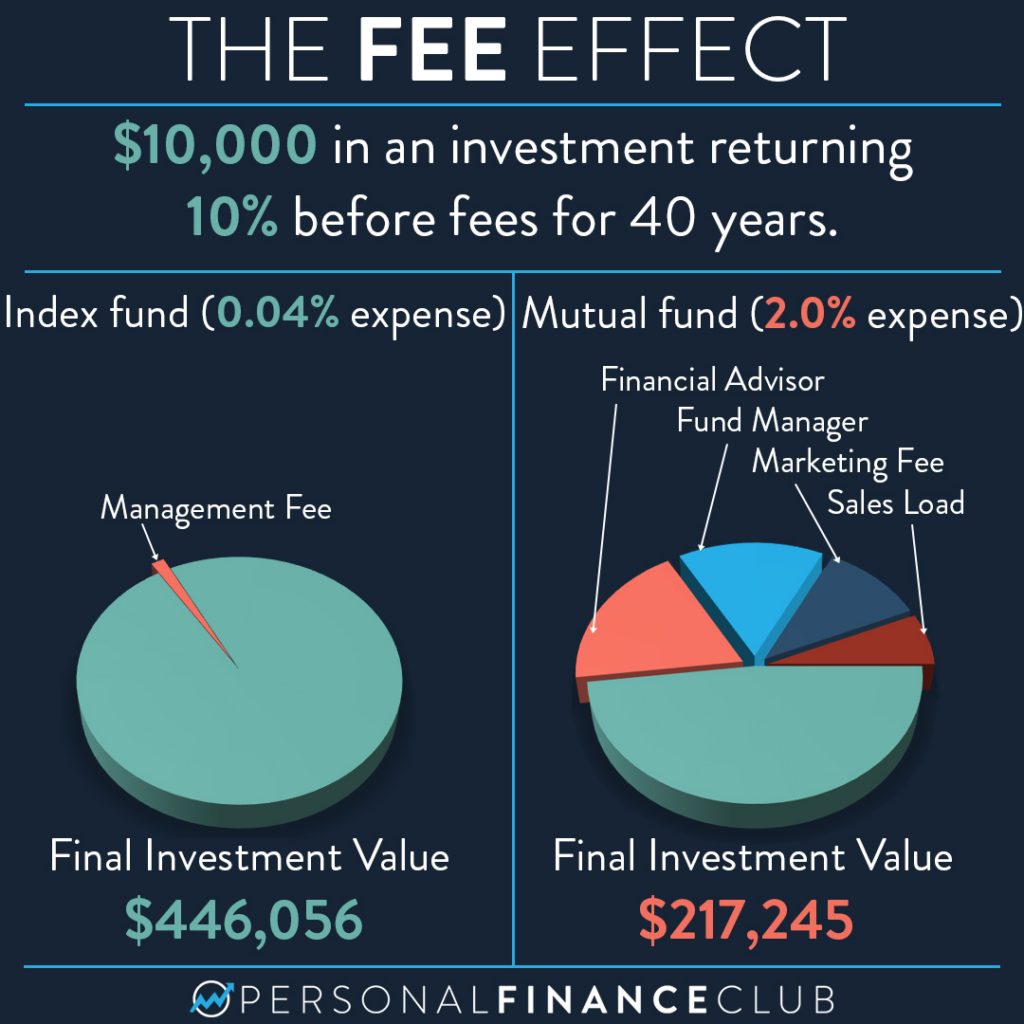

LADS investing means keeping your investments Low-cost, Automatic, Diversified, and Simple. If an investment does not meet these 4 criteria, it is not considered suitable for clients of Simple Money.

Low-cost

Fees are rampant in the financial advice and investing industry. It’s hard enough making a return—don’t give your hard-earned returns to your adviser.

Automatic

We want to create money and wealth-building systems that require minimal human input, so that our money is working for us, and not the other way around.

Diversified

We don’t put all our eggs in one basket. By diversifying, we reduce the risk of failure and increase your chance of achieving your financial goals.

Simple

We create systems that are easy to understand and maintain. Complexity adds stress and rarely performs as well as simple, disciplined systems.

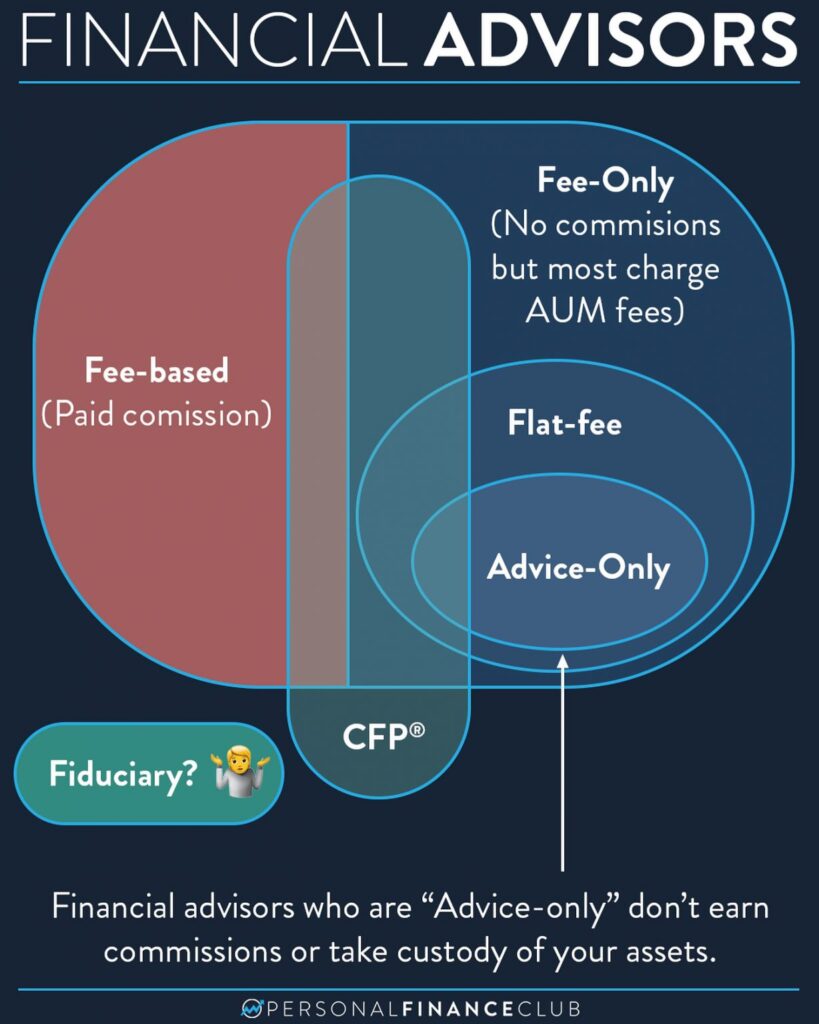

What is a “fee-only” financial adviser?

New Zealand financial advisers have 3 common compensation models:

- Commission based: you’ll often see these advisers offering “free financial advise” but it’s going to cost you a lot in the long run. The advisers are compensated by the products they recommend, not by you. This is Economics 101: The incentives are misaligned. A commissioned advisor now has an incentive to recommend the product that pays the highest commission, not the product that’s most suitable to you.

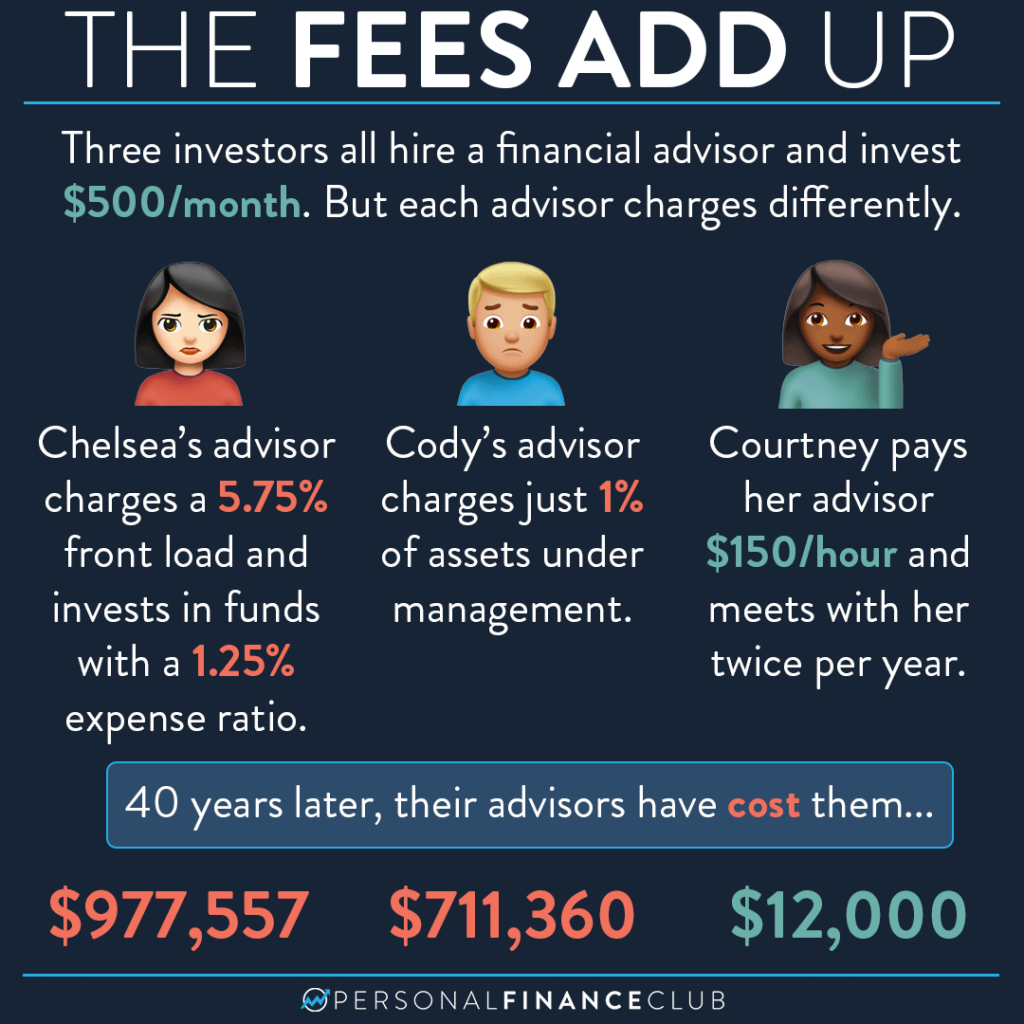

- Asset under management (AUM): These advisers charge a percentage of your portfolio. They often won’t work with investors who are just getting started, as they need a minimum about of investments to justify working with you. For example, they might not want to work with you if you have less than $500,000 in investable assets, since if they charge a 1% annual fee that will bring in less than $5,000 into their firm annually.

While there is an incentive to grow your portfolio so the adviser firm can take the same percentage of a higher amount, in reality advisers have very little control over investment performance. - Fee-only: This is the simplest and most consumer friendly compensation model. Rather than paying a percentage of your asset or the adviser, you simply pay your adviser to provide you with advise on your specific situation. The adviser is only compensated by you, so they only work for you. The incentives are aligned that they want to give you the best advise possible. In the long run, this is the lowest financial advise cost to the consumer

Commission Based Advise

Commission based advisers might offer “free” financial advice. But that’s because you’re the product. Always check the disclosures and terms and conditions.

For example, it may say something like: “We only provide financial advice about products from certain providers. Our KiwiSaver and Wealth product providers are…”

Or “For some KiwiSaver’s, our company receives commissions from the providers with whom we arrange those products. If you decide to move your KiwiSaver from one provider to one of ours upon our advice, the provider will pay our company a commission.”

I’m not sure how these advisers can say with a straight face that they are putting their clients interest first, when they are being compensated for recommending certain products. It really makes the conflict of interests difficult to manage.

Asset Under Management

Again, in this model you might receive “free” advice, but only if the advisers are allowed to manage your money. They’ll collect an “asset under management” fee, which funds their advising business.

The good thing about this model is the advisers have an incentive to increase your funds. After all, if they are collecting 1% of your assets in fees, then the more money you have, the more fees they make!

However, you don’t need to pay 1% a year for your money to be managed. In fact, you can probably do it yourself with a little advise and coaching.

You can compare the costs of New Zealand investments with our free calculator.

Our Model: Fee- and Advice Only or How to Save $1,000,000

Rather than make it confusing about who’s paying who and how I’m getting paid, let’s make it simple.

You pay me. I give you specific advice to your situation. That keeps things tidy and Simple. You know that I’m working for your best interests and I don’t have any incentive to provide you anything other than the best advice possible.

Any other model has too many ethical pitfalls, gets too expensive, or has potentially mis-aligned incentives. Fee for service is the simplest renumeration schedule and I’m proud to be one of the few financial advisers in New Zealand to use it.